This paper attempts to design and test empirical

models, which integrate theoretical, institutional, and other factors, which

interact to explain ownership structure. Ex-ante information at the level of

underpricing succeeds the Indian stock market crunch. The study is based on IPO

that listed at Bombay stock exchange given that April 2000 to December 2011.

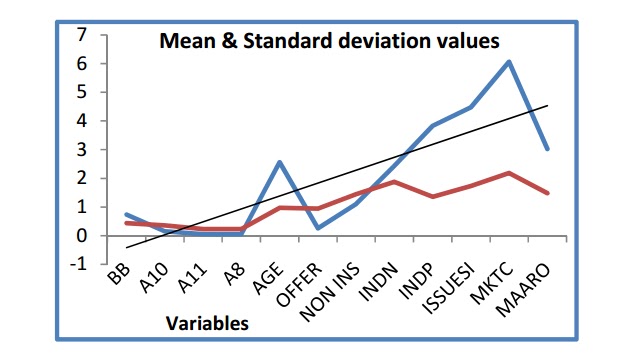

Multiple linear regressions are used to distinguish the relationship between

various independent variables with the dependent variable, i.e. level of

underpricing. The outcomes of multiple regressions reveal that, firm’s age, IPO

years, book building pricing mechanism, ownership structure, issue size, &

market capitalization explained 44% of the variation in issuer underpricing,

Durbin Watson’s value subsisted 1.58, which indicates that, there is a positive

sequential relationship between variables. Number of share offered, issue size,

market capitalization, subscription offer timing, book building mechanism and

IPO years 2006, 2009 & 2011 are constructed to have important effect on the

level of underpricing after the Indian market crisis. Nevertheless, firm’s age,

IPOs year 2008, private issuing firms, non institutional promoters, Indian

promoters and non institutional non promoters contain no significant difference

in the level of underpricing after-market crisis.

Article by Rohit

Bansal and Ashu Khanna,from Institute of Technology, Roorkee Uttrakhand, India

Full access: http://mrw.so/jHZzF

评论

发表评论